As mortgage interest rates continue to climb, mortgage refinancing applications remain in decline after refinancing exploded in 2020 and 2021 during the pandemic.

Most commonly, mortgage refinancing allows a homeowner to replace their existing loan with a new loan at a lower interest rate or different term length. Certain types of refinancing agreements can also enable the homeowner to receive cash in exchange for accrued home equity. The mortgage refinance industry is acutely sensitive to changes in the overall U.S. economy, so as economic conditions continue to change, the mortgage refinancing landscape will shift as well.

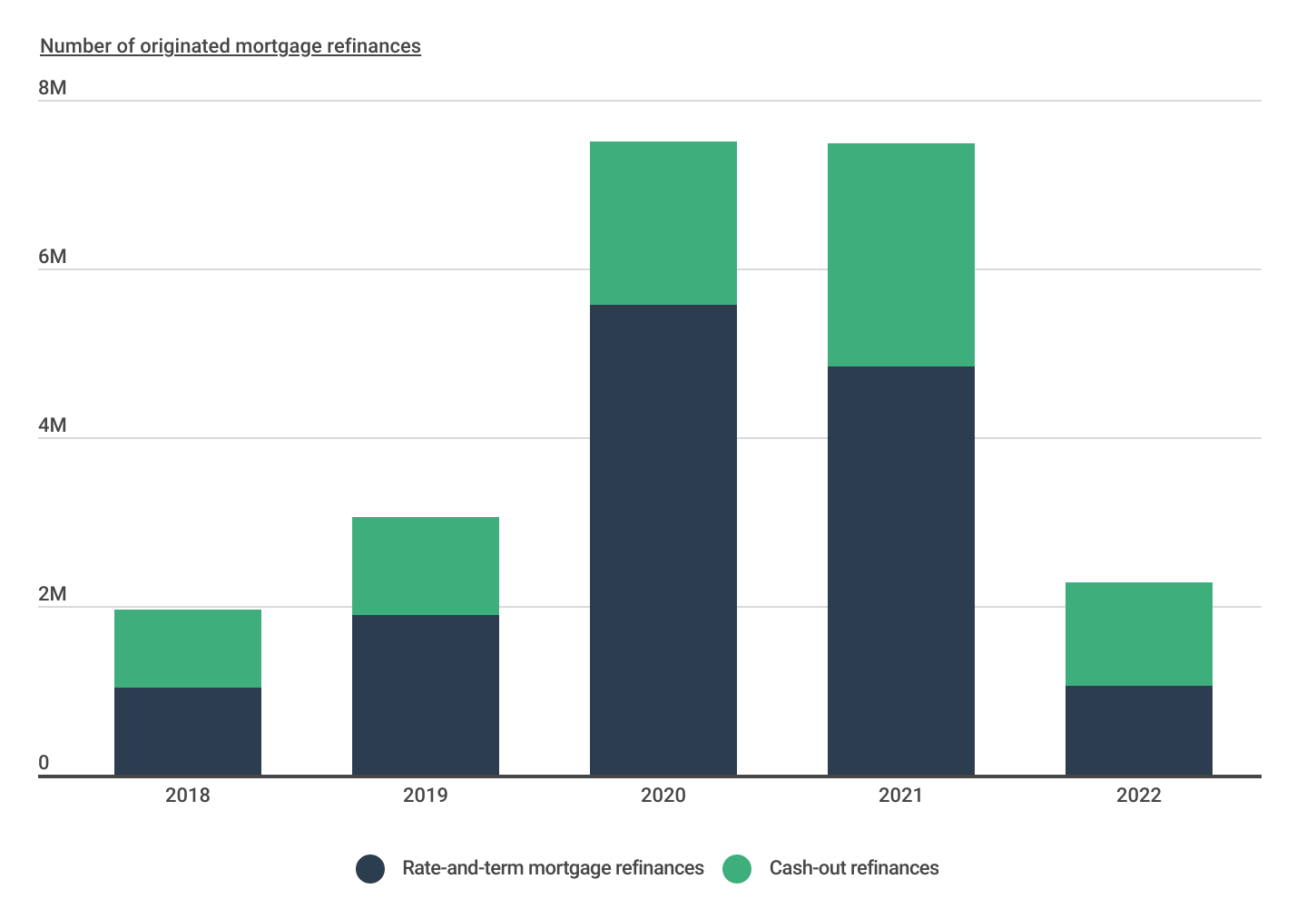

Composition of U.S. Mortgage Refinances

Mortgage refinances returned to pre-pandemic levels in 2022, but a majority of them were cash-out

Source: Construction Coverage analysis of Home Mortgage Disclosure Act data | Image Credit: Construction Coverage

Due primarily to historically low interest rates, mortgage refinances skyrocketed in 2020, increasing a whopping 145% from 2019 and remaining at similar levels in 2021. However, in 2022, mortgage refinances regressed back to pre-pandemic levels—declining nearly 70% to a total of approximately 2.3 million refinances. Notably, the composition of mortgage refinances shifted as well. Driven by a historic runup in home sale value during COVID, nearly 54% of all mortgage refinances in 2022 were cash-out as homeowners looked to draw on their newfound home equity.

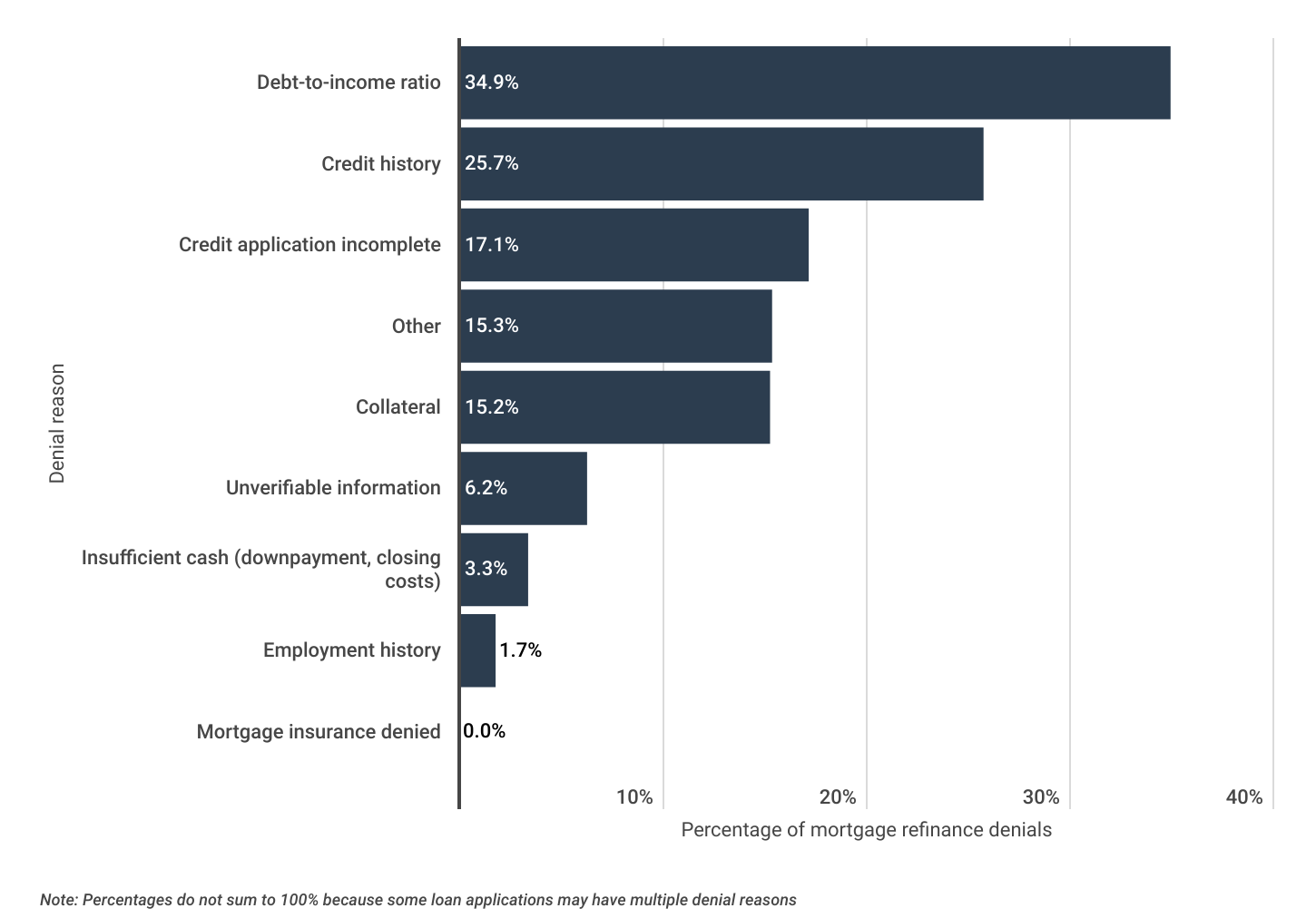

Most Common Denial Reasons for Mortgage Refinance Applications

Inadequate debt-to-income ratio is the most common reason for denied refinancing

Source: Construction Coverage analysis of Home Mortgage Disclosure Act data | Image Credit: Construction Coverage

Although refinancing a mortgage can help reduce monthly payments or provide some much needed liquidity, not all refinancing applications are approved. The most common reason for refinancing denials was an inadequate debt-to-income ratio, cited in nearly 35% of all refinancing applications that were denied. Credit history was the second most common reason for refinancing denials, mentioned in over one in four denials.

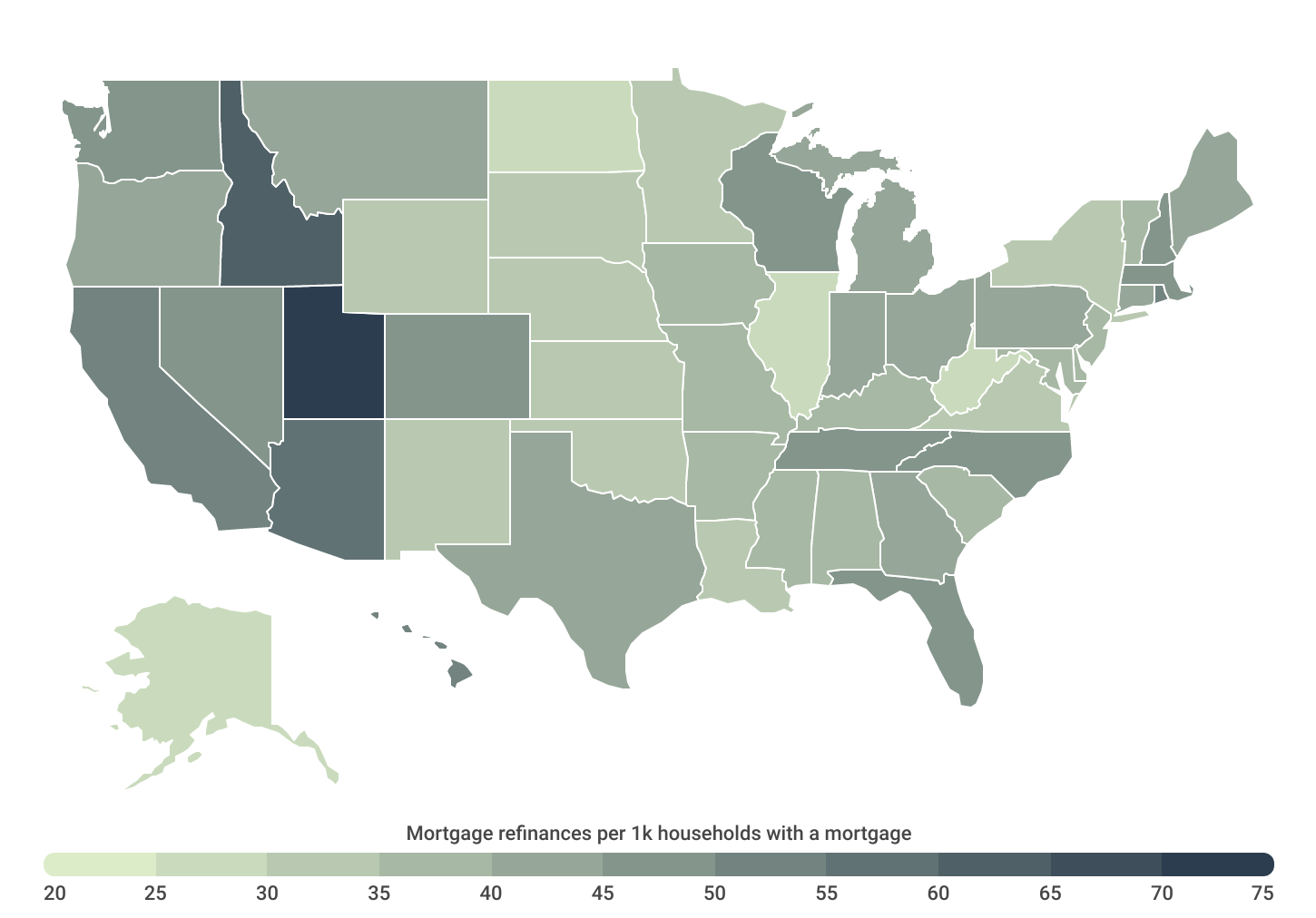

Mortgage Refinances by Location

Mortgage refinancing is most popular in Utah, Idaho, and Arizona

Source: Construction Coverage analysis of Home Mortgage Disclosure Act data | Image Credit: Construction Coverage

The proportion of households that refinance their mortgage varies considerably across regions of the country. In the U.S. overall, there were 42.1 mortgage refinances approved per 1,000 households with mortgages in 2022. Refinancing is much more common in the western U.S. where home prices have appreciated rapidly over the past decade. Out of all 50 states, Utah had the most mortgage refinances at 70.3 refinances per 1,000 households with a mortgage, followed by Idaho (63.4), and Arizona (56.2). Conversely, at just 26.0 refinances per 1,000 mortgaged households, Alaska had the fewest.

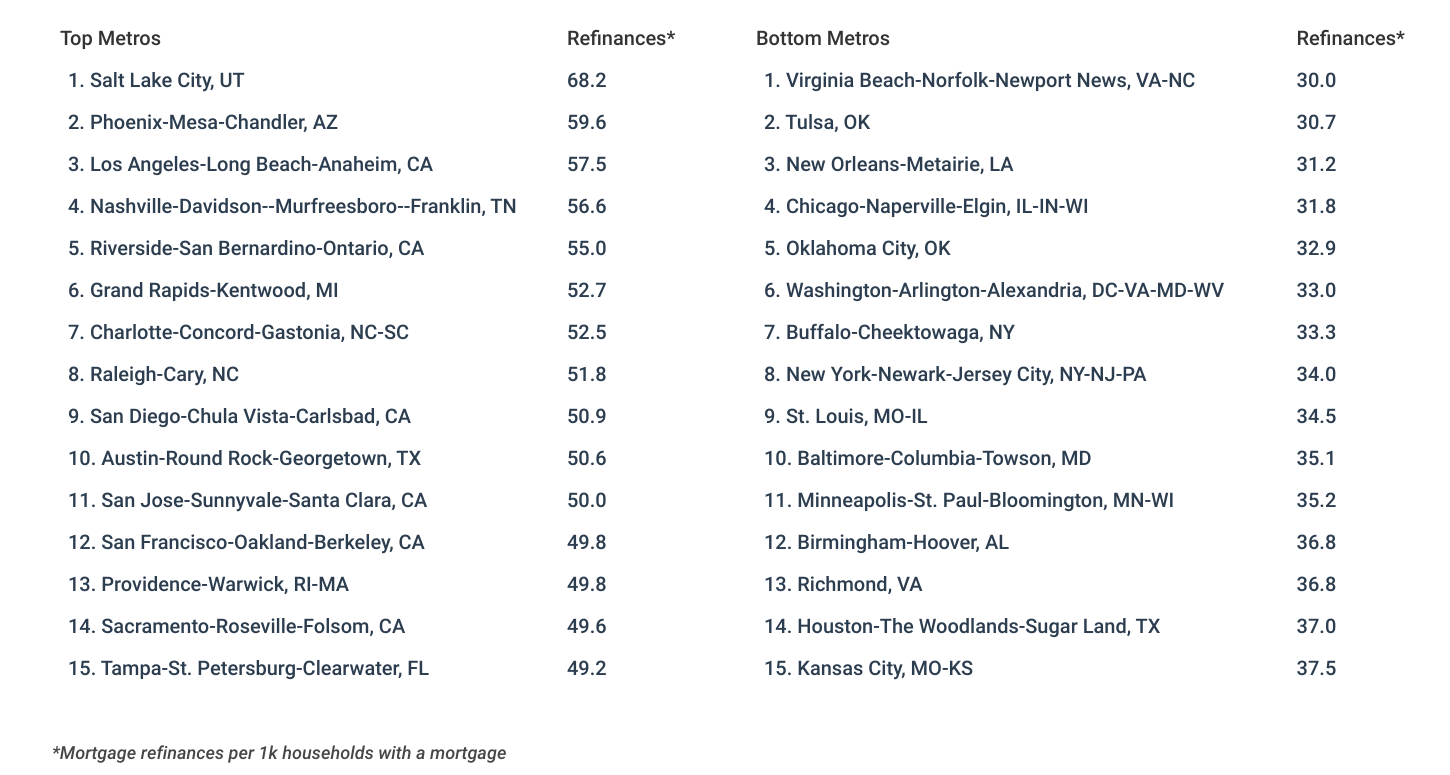

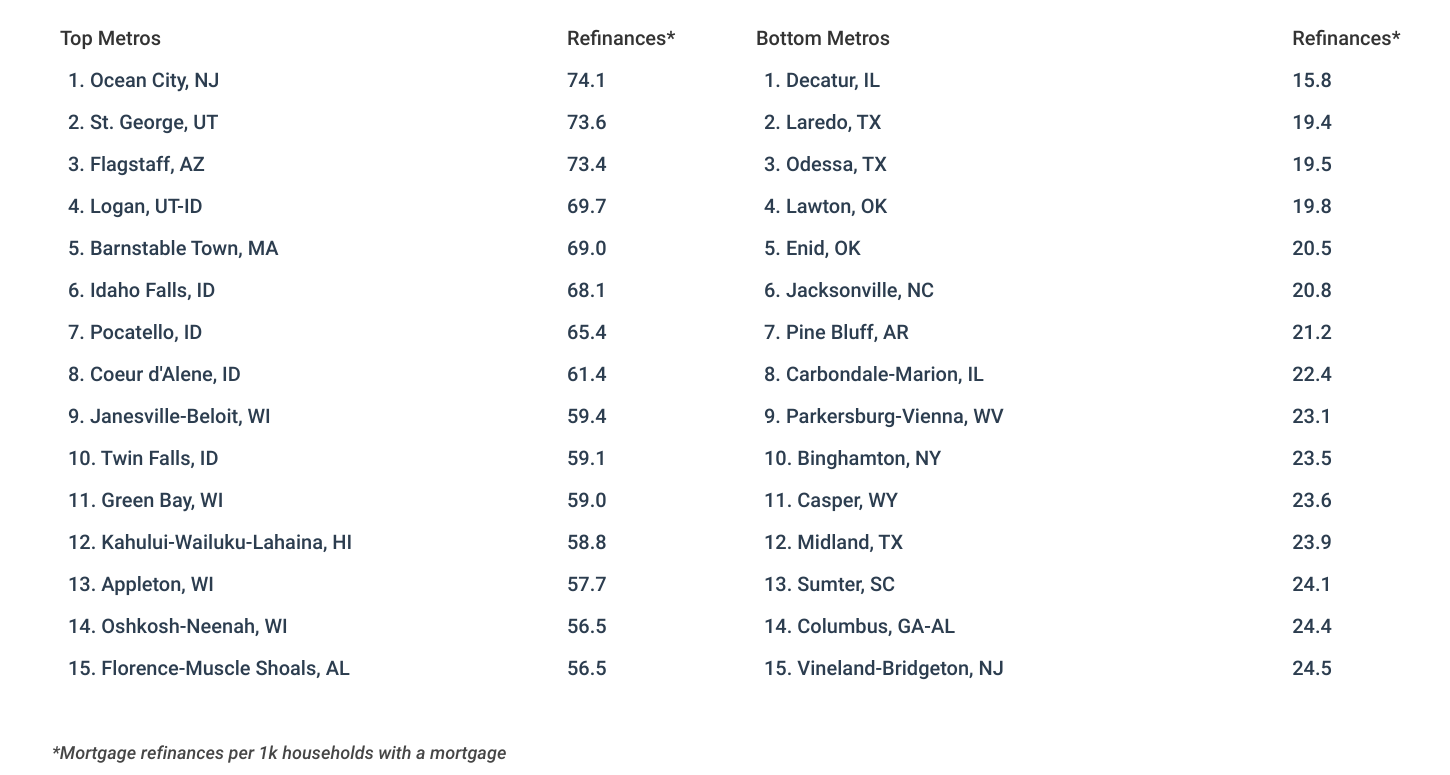

At the metropolitan level, many of the same trends hold true. Utah is well represented, with the Salt Lake City metro ranking first among large metros, Provo-Orem claiming the top spot among midsize metros, and St. George, UT and Logan, UT-ID ranking second and fourth, respectively, among small metros.

Below is a complete breakdown of mortgage refinances in 2022 across more than 380 metropolitan areas, grouped by size, and all 50 states. The analysis was conducted by researchers at Construction Coverage, a website that compares construction software and insurance, using data from the Federal Financial Institutions Examination Council and the U.S. Census Bureau. For more information on how each statistic was computed, refer to the methodology section below.

Large Metros With the Most Mortgage Refinances

Midsize Metros With the Most Mortgage Refinances

Small Metros With the Most Mortgage Refinances

States With the Most Mortgage Refinances

Methodology

Photo Credit: Rawpixel.com / Shutterstock

To find the locations with the most mortgage refinances, researchers at Construction Coverage analyzed the latest data from the Federal Financial Institutions Examination Council’s 2022 Home Mortgage Disclosure Act and the U.S. Census Bureau’s 2022 American Community Survey. The researchers ranked metros according to the number of mortgage refinances originated in 2022 per 1,000 households with a mortgage. Only conventional refinances for single family dwellings were considered for this analysis. In the event of a tie, the metro with the larger total number of mortgage refinances was ranked higher.

To improve relevance, metropolitan areas were grouped in to the following cohorts based on population size:

- Small metros: less than 350,000

- Midsize metros: 350,000–999,999

- Large metros: 1,000,000 or more

For complete results, see U.S. Cities With the Most Mortgage Refinances on Construction Coverage.